For an online business, what types of insurance are really useful (cyber, liability, merchandise)? What do experts in the field recommend in 2026?

We live in the most dynamic era of online commerce ever. In 2026, the boundaries between digital and physical have almost disappeared, and the opportunities to scale a business across borders are greater than ever. In fact, a niche store in Romania can now reach customers’ homes on three continents with just a few clicks.

But with this success and the incredible speed of transactions, new challenges have also emerged. In a hyper-connected world, security is no longer just a checkmark on the IT department’s list, but has become the foundation on which you build your reputation and the future of your brand.

But what does it really mean to be “protected” in today’s landscape? Experts in the field agree: in 2026, it’s no longer about whether you’ll encounter a digital or logistical obstacle, but about how prepared you are to overcome it without your business suffering.

In fact, to put things into perspective, we will analyze the services of Leader Team Broker, the team that brought to Romania the first policies dedicated to cyber risks. With over 20 years of experience and a solid presence on the international market (including at the famous Lloyd’s of London), they will help us filter the noise and identify those IT insurance or professional civil liability that transforms a potential crisis into a simple stage to manage.

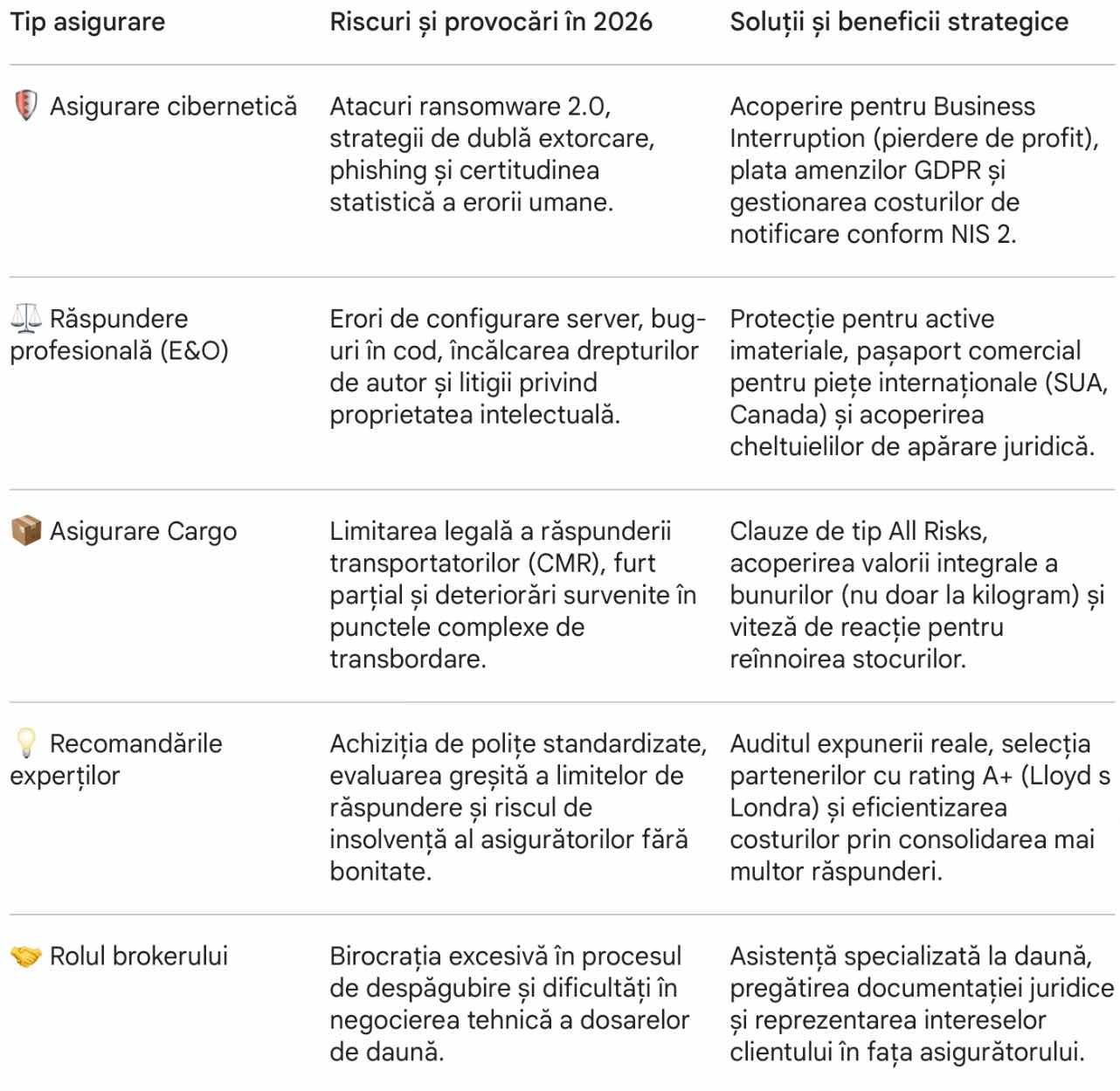

Cyber-resilience in 2026: From a hypothetical risk to a statistical certainty

The concept of cybersecurity has gone beyond the technical sphere of IT departments, becoming in 2026 a critical variable in the financial balance of any company with online activity. In an environment where automated attacks target infrastructure without discriminating according to the size of the organization, cyber insurance is the main tool for transferring residual risk.

Evolution of threats: Ransomware 2.0 and social engineering

Currently, ransomware incidents are no longer limited to simple data encryption. “Double extortion” strategies now include exfiltrating sensitive information and threatening to publish it, which generates irreparable reputational damage.

Global statistics indicate a high frequency of phishing attempts, which remain the main gateway into corporate networks. Despite investments in firewalls and endpoint solutions, human error remains a constant vulnerability, turning security incidents into a statistical certainty in the medium term.

Business Interruption: The Impact on Cash Flow

The most costly component of a cyberattack is not the actual recovery of data, but the interruption of economic activity (Business Interruption). For an online business, every hour of unavailability of the platform translates into direct loss of revenue and fixed costs that continue to accumulate.

A market-adapted insurance policy from 2026 covers the decrease in profit margin and the additional operational expenses necessary to maintain activity during the system restoration period. These financial instruments are calibrated to protect the company’s liquidity in a moment of operational crisis.

Legal framework and compliance: NIS 2 and GDPR sanctions

The year 2026 marks the maturity of the application of the NIS 2 Directive at European level, which imposes rigorous digital resilience standards for a wide range of sectors. Companies that manage user data are subject to double pressure: the technical need for protection and the legal obligation to report and comply.

- Administrative fines: Specialized insurance can cover the costs related to authorities’ investigations and GDPR fines, where the legislation allows.

- Incident notification: The process of notifying affected customers involves significant logistical and legal costs, often fully covered by the insurance mechanism.

Professional Liability: The Financial Shield Against Execution Errors in 2026

In the digital economy of 2026, where the finished product is often intangible – source code, data strategies or cloud services – the distinction between a minor error and major financial damage has become extremely fine. Professional Liability Insurance, known internationally as Errors & Omissions (E&O), is a standard of operational integrity. This covers legal liability arising from human error, negligence or failure to deliver services to the promised contractual standards.

Technical errors and omissions with financial impact

The complexity of integrated systems means that a simple server configuration error or a “bug” in a payment processing script can generate cascading losses for end customers. In such scenarios, injured customers will not only seek technical remediation, but also full recovery of lost revenue during the incident.

E&O policy intervenes precisely at this critical point, covering legal defense expenses and, more importantly, the compensation that the company would have to pay to cover pure financial damages suffered by third parties. Without this mechanism, a single court action can deplete the working capital of an agency or SaaS service provider.

Intellectual property in the digital ecosystem

With the saturation of digital content and the widespread use of generation algorithms, the risks related to copyright infringement have multiplied. In 2026, allegations of unauthorized use of digital assets or unintentional infringement of software patents are increasingly common.

Intellectual property disputes are among the most expensive and time-consuming commercial processes. Professional liability insurance provides the financial resources necessary to manage these disputes, protecting the business against legal costs and damages that may result from the erroneous use of protected materials.

A mandatory condition for access to foreign markets

Beyond internal protection, this insurance has become a veritable “commercial passport”. For online businesses targeting markets such as the US, Canada or the European Union, having a professional liability policy with specific limits is a standard clause in most collaboration contracts.

- Procurement Standards: Large corporations and marketplace platforms often refuse to enroll suppliers who cannot provide proof of E&O coverage.

- Contractual Risk Transfer: External partners require this insurance to ensure that any performance error can be financially compensated by a reputable insurer, eliminating the risk of supplier insolvency in the event of litigation.

Cargo Insurance: Cargo Safety from Warehouse to Customer Door in 2026

For any online business that sells physical goods, transit represents the interval with the greatest exposure to uncontrollable external factors. Although logistics have become much more efficient, the complexity of supply chains in 2026 involves multiple transhipment points, where product integrity can be compromised. A common strategic mistake is to rely exclusively on the insurance of the carrier or courier company, underestimating the legal limitations of their liability.

The trap of limited carrier liability

By default, the liability of road, sea or air carriers is regulated by international conventions (such as the CMR Convention) that cap compensation based on the weight of the cargo, not its actual invoice value. In the case of high-value-added products and low weight – from electronics to fashion items – this limitation leaves a significant part of the invested capital uncovered.

Cargo insurance transfers this risk from the company’s balance sheet to the insurer, guaranteeing coverage of the full value of the goods, including taxes and expected profit, regardless of the liability limits of the transport company.

“All Risks” clauses and operational continuity

Unlike basic insurance that covers only catastrophic events, a modern Cargo policy operates on the “All Risks” principle. It provides protection against a wide range of incidents: from damage during handling and unloading, to partial theft or accidental loss in intermediate warehouses.

The major advantage is not only financial, but also operational. In the event of an incident affecting an entire batch of goods, the process of recovering damage through your own insurance is much faster than a prolonged dispute with the carrier. This speed of reaction allows for immediate replenishment of stocks and fulfillment of customer orders, maintaining the stability of cash flow and brand reputation.

Contractual flexibility and adaptability

In 2026, the structure of transport policies has adapted to the dynamism of e-commerce, offering scalable solutions depending on the volume and frequency of deliveries:

- Open Covers: Intended for companies with constant activity, these automatically insure all shipments made in a year, eliminating the bureaucracy of declaring each package.

- Individual transport insurance: Ideal for high-value deliveries or occasional shipments, offering precise control over costs.

Regardless of the final destination of the products, integrating Cargo insurance into the supply chain strategy transforms logistics from a vulnerability into a controlled process.

Cyber, Liability and Cargo: Expert Recommendations for 2026

Choosing an insurance portfolio for an online business has ceased to be a reactive procurement process. In 2026, risk management experts recommend a proactive approach, where the policy is viewed as a financial balance instrument, not as a simple contractual obligation. The selection decision must be based on the analysis of the real exposure and the creditworthiness of the insurance partners.

Exposure audit and coverage customization

The first recommendation of the specialists aims to carry out a rigorous audit of digital and logistics assets. An online business cannot operate efficiently with “standardized” insurance solutions, because the risks of a marketplace store are fundamentally different from those of a cloud infrastructure provider.

It is essential that liability limits are calculated according to the volume of data processed and the value of daily transactions. Experts emphasize the importance of modularized clauses, which allow the addition or elimination of specific risks (for example, extending coverage to foreign markets such as the USA), thus avoiding paying premiums for risks that do not exist in the respective business model.

Solvency Criterion: The Importance of an A+ Rating

Given that the global market is marked by volatility, the insurer’s ability to honor large-scale claims is the most important indicator of trust. The unanimous recommendation of consultants in 2026 is to focus on insurance markets with a higher rating (A+), such as the Lloyd’s of London market.

A high rating provides certainty that, in the event of a systemic incident, such as a security breach affecting multiple providers simultaneously, the insurer has the capital reserves necessary for rapid compensation. The insurer’s creditworthiness is, in effect, the guarantee that the risk transfer is real and not just a formal document.

The role of the broker in claim management

The effectiveness of insurance is measured exclusively at the time of the insured event. Experts recommend working with specialized brokers who provide technical assistance throughout the entire claim process.

The difference between a quick financial recovery and a lengthy bureaucratic process lies in the broker’s ability to negotiate with the insurer and prepare the necessary documentation in a correct technical language. In 2026, the added value of a broker is no longer just sales mediation, but consulting expertise in critical moments of operational crisis.

Optimizing costs by consolidating liabilities

A recommended financial strategy for streamlining protection budgets is to consolidate several types of liabilities on a single insurance platform. This method not only simplifies portfolio management, but also allows for preferential commercial conditions.

By bundling Cyber, E&O and Cargo insurance, a company can achieve significant premium reductions while maintaining a high level of protection. This integrated approach ensures the elimination of “gray areas” in contracts, where certain risks could remain uncovered due to faulty overlaps between different policies.

For an online business, which types of insurance are really useful (cyber, liability, cargo)? – useful tips for entrepreneurs in 2026

Leader Team Broker: Expertise that makes the difference for online businesses in 2026

Leader Team Broker: Expertise that makes the difference for online businesses in 2026

When the continuity of a business is at stake, the experience and creditworthiness of the insurance partner become the only critical variables. Leader Team Broker, a company founded in 2007 in Bucharest, has positioned itself from the beginning as an innovator on the Romanian market in this field. Being among the first brokers to use RPA (Robotic Process Automation) technology and the absolute pioneer in promoting Cyber Risk and IT insurance in Romania, the brand today represents a benchmark for specialized consulting.

A unique business architecture: Consulting, not just distribution

In 2026, Leader Team’s major differentiator lies in its working methodology. The business model it approaches balances policy distribution with in-depth risk management consulting. Instead of offering standardized products, the team analyzes the specifics of each client to design a personalized strategy. This approach allows for the coverage of complex risks, often refused or ignored by general insurers.

Access to Lloyd’s market and A+ safety rating

A decisive argument for companies operating internationally is Leader Team’s strategic partnership with Lloyd’s market in London. This collaboration gives Romanian clients access to the resources of 85 elite insurers on the London market, rated “A+” by Standard & Poor’s and Fitch Ratings.

The result? A policy issued through Leader Team is recognized and accepted unconditionally anywhere in the world – from major trading partners in the US and Canada, to giants like Amazon, which impose rigorous insurance standards on their partners.

Cost Optimization: Up to 60% Savings through Consolidation

Financial efficiency is one of the main reasons why entrepreneurs choose Leader Team in 2026. Our team of brokers has the unique ability to combine multiple types of liability (Cyber, IT Professional Liability, General Liability) on a single policy. This consolidation of products can generate a reduction in total costs of up to 60%, while providing over 50% more coverage than similar products on the local market.

Digital Speed and Internal Claims Support

In an economy where speed of response is vital, Leader Team has eliminated excessive bureaucracy:

- Ultra-fast quotes: The process is simplified through intuitive questionnaires, and clients can receive a personalized offer within 24-48 hours (and in standard cases, even within 30 minutes).

- Dedicated claims department: Unlike a simple intermediary, Leader Team Broker has an internal claims support structure. Our specialists take over the management of the file and represent the client’s interests in the relationship with the insurer, ensuring a correct and fast settlement of the money.

A complete portfolio for any stage of development

Although recognized as a leader in Cyber and IT insurance, Leader Team Broker’s expertise covers the entire spectrum of an organization’s needs. The portfolio includes solutions for goods and equipment, car fleets, transport insurance (Cargo/CMR), but also employee benefits (international health insurance through partners such as AXA or Bupa and life insurance).

In short, collaborating with a broker who understands modern technology and risks, such as Leader Team Broker, transforms uncertainty into a controlled risk factor, providing the peace of mind necessary to scale the business safely.

In conclusion, in 2026, online success is no longer measured only in turnover, but in the business’s ability to remain standing in the face of an unforeseen incident. The difference between a brand that disappears after the first cyberattack and one that thrives is given by the way the risks are transferred to trusted partners.

Choosing the right mix of insurance, from Cyber insurance and specific IT insurance policies to professional civil liability, is an investment in stability. Working with a broker who understands the architecture of modern risks, like Leader Team Broker, gives you the certainty that, no matter where the market or technology evolves, the foundation of your business remains protected.

Real security comes from a solid partnership, which allows you to shift your focus from “what could go wrong” to “how we can grow further.”

Frequently asked questions about useful insurance for online businesses in 2026

What exactly does cyber insurance cover in the event of a ransomware attack?

A modern cyber policy is not limited to data recovery. It covers the costs of cybercrime experts, the payment of any GDPR fines derived from the security breach and, most importantly, the loss of profit suffered during the period in which the activity was interrupted. It also covers the PR expenses necessary to communicate transparently with customers and protect the brand’s reputation.

Why is professional liability (E&O) insurance a requirement for international contracts?

Trading partners in the USA, Canada or the European Union require this policy as a guarantee of your creditworthiness. It confirms that, in the event of an execution error, a software bug or an omission that causes them financial losses, there is an insurer with a high rating (A+) that can cover the compensation. Without this protection, the risk of a supplier’s insolvency in the event of a dispute is too high for large corporations.

If the carrier already has insurance, why do I need a Cargo policy?

Carrier insurance (CMR) is limited by international conventions to a fixed amount per kilogram, which often does not even cover 10% of the value of expensive and lightweight products such as electronics. A separate Cargo insurance provides protection for the actual value of the goods and includes All Risks clauses, offering much faster compensation, without having to rely on lengthy processes to establish the carrier’s fault.

How to optimize insurance costs for an online startup?

The most effective method in 2026 is to consolidate risks. Instead of purchasing separate policies for cyber, cargo, and professional liability, you can opt for an integrated solution. Leader Team Broker experts can reduce insurance premiums by up to 60% by grouping these liabilities under a single contractual umbrella, while eliminating unnecessary cost overlaps.

What if I need quick assistance in case of damage?

Unlike automated platforms, working with a specialized broker gives you access to an in-house claims department. The moment you notify an incident, consultants immediately take over communication with the insurer, prepare technical documentation, and negotiate on your behalf to ensure that you receive the correct compensation in the shortest possible time.